Tags

Education, Invest, Investing, Investments, iron butterfly, Loss, Money, Options, options strategies, Profit, reverse iron butterfly, Risk, Stock, Stocks, Strategy, Strike Price, Think

Whereas last week I covered a strategy that an investor would use when a low degree of volatility is expected, this week I will be going over a strategy that could be employed when there are expectations of heavy volatility for a stock. The Reverse Iron Butterfly is the exact opposite of the Iron Butterfly strategy. It is a strategy that would be used if an investor expects the stock to move a lot before the expiration date, but is not sure about which way it may go.

This strategy could be optimal for a stock that is expected to release some very large news or may have an important earnings release date coming up, as the stock could move drastically based on investor interpretation and response to this news. In order to complete a Reverse Iron Condor, an investor would:

- Sell a lower strike out-of-the-money put

- Buy a middle strike at-the-money put

- Buy another middle strike at-the-money call

- Sell another higher strike out-of-the-money call

Maximum Loss:

Because the investor has sold puts and calls that are further out of the money (and therefore would have lower premiums) and bough higher premium puts and calls that are at the money, he or she would have spent more on buying than gained on selling, and therefore would have an initial payout as compared to a normal Iron Butterfly where they would have had an initial input of cash. This initial payout at the at the money strike, is also the maximum loss obtained for the investor. If the options expire at the original price, then the maximum loss would be achieved.

Any movement away from the initial at the money price in either direction would see the loss decline and move the investor towards positive territory.

Example – Ford

For this example we will use Ford and their current options for June 17th, 2016. As of closing April 5th, 2016 the current price of Ford is $12.77. For ease, the price of Ford will be rounded up to $13. We will use quantities of 1000 for each option. An investor performing a Reverse Iron Butterfly on Ford could:

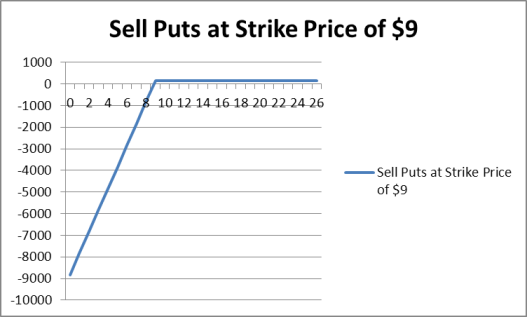

- Sell 1000 puts at a strike price of $9 at premium of $0.16 for a total inflow of $160

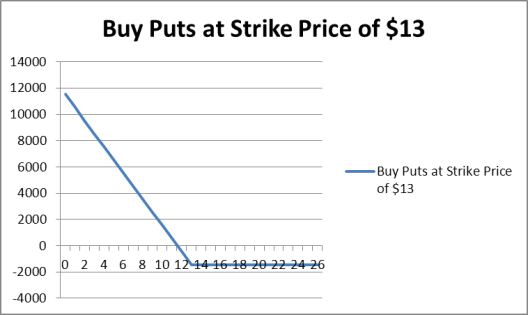

2. Buy 1000 puts at a strike price of $13 at premium of $1.46 for total outflow of $1,460

2. Buy 1000 puts at a strike price of $13 at premium of $1.46 for total outflow of $1,460

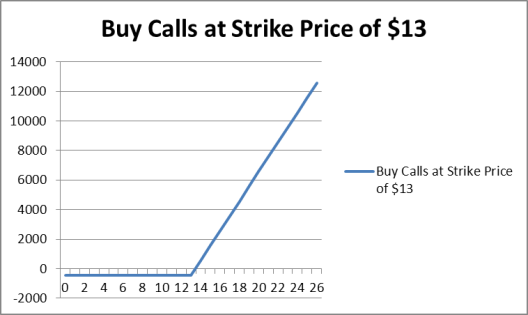

3. Buy 1000 calls at a strike price of $13 at premium of $0.44 for total outflow of $440

4. Sell 1000 calls at a strike price of $17 at premium of $0.02 for total inflow of $20

4. Sell 1000 calls at a strike price of $17 at premium of $0.02 for total inflow of $20

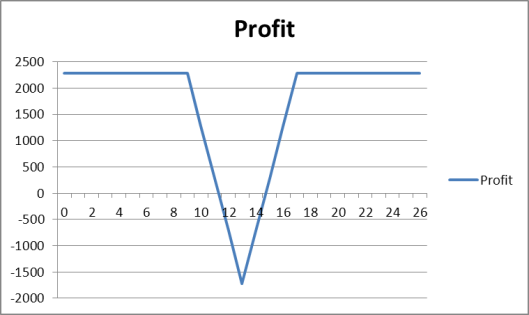

This would give the investor an initial outflow of $1,720 ($1,900-180). The investor’s maximum loss for this strategy on Ford would therefore be the same $1,720. This would occur if at expiration the price of the stock is $13.

Maximum Profit:

On an ordinary Reveres Iron Butterfly, the maximum profit would occur if the price at expiration is either equal to or less than the sold put, or equal to or greater than the sold call. The Maximum profit would thus occur at $17 or over of at $9 or below. The maximum profit for this strategy would be $2,280. Although this seems like a decent strategy if you expect the stock to have high volatility, it is necessary to analyze the premiums and see if this is truly the best strategy before selecting it.

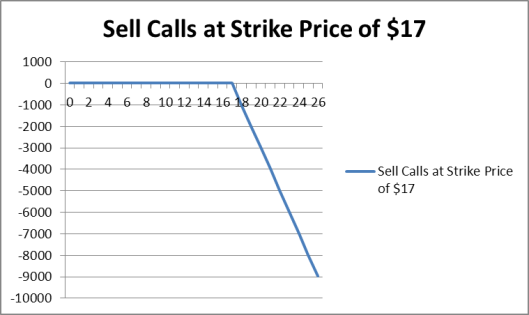

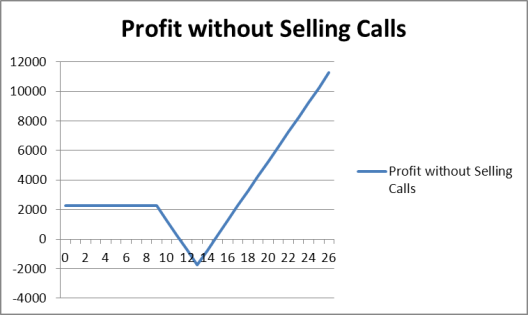

In this situation, because the difference between the premium on the sold put and premium on the bough put is much larger than the difference between the premium on the sold call and the premium on the bought call, this strategy may not be the most efficient. The sold put is the same price away from the bought put ($4) as the sold call is away from the bought call, but the difference in premiums is much less. This shows that it is likely that investors believe that Ford is much more likely to drop $4 than to increase $4. When analyzing the strategy, it seems pointless in this situation to sell the calls. Because the premium is so low, only $20 would be gained from performing this part of the strategy, and the possible losses if the price is to rise above $17 quickly eliminates the initial inflow of $20. In fact, this only raises the maximum loss by $20 and gives the investor unlimited gain if the price of the stock is to increase. This is demonstrated below.

It thus may be better based on Ford´s options to attempt a different strategy. Although the Reverse Iron Butterfly could be a way to take advantage of expected volatility for Ford, other strategies may work better as well!

Break Even Points (BEPS)

The breakeven points for the Reverse Iron Butterfly can be calculated using the following formulae.

For the upper breakeven point you can take the strike price of the long call and add the net premium paid.

- $13.00+$1.74(per share net premium) = $14.74

For the lower breakeven point you can take the strike price of the long put and subtract the net premium paid.

- $13.00-$1.74(per share net premium) = $11.26

Conclusion:

The Reverse Iron Butterfly is a very useful strategy that can be used when high volatility is expected for a stock. However, as we have seen it may not always be the best strategy so it is wise to analyze completely before selecting an investing strategy. This was definitely the case in Ford due to obvious investor sentiment that the stock is not worth $17. Be careful when selecting options strategies, as the market can dictate their usefulness in more ways than one!