Tags

Airlines, American Airliens, American Airlines, Diversification, ETF's, Hedging, Heding, Investing, Jet Blue, Loss, Money, Oil, Profit, Spirit Airlines, Stocks, Strategy, Think

Oil prices have been an extremely hot topic over the last couple months, with differing opinions flying about all over the place. Over the past year, oil has seen historic falls and has gone continued to go lower and lower. Over the last few days, oil prices have increased amid a rally, but how long will this rally really last? Morgan Stanley believes that this rally will not last much longer and that prices will even go lower in the first half of 2015. They believe that Q2 will see the greatest decline with oil prices falling as low as $43 in Q2 of this year. For value investors, this drop in oil prices is a fantastic opportunity to buy, but the question remains…. When should we buy?

Investors believed it was undervalued when prices fell into the 60’s, but prices have just kept on dropping and the early birds are now sitting at pretty decently sized losses. Personally, I do not think that a commodity such as oil has any chance at sustaining this level of prices for an extended period of time, but it is not unreasonable to imagine that prices may hover under the 60’s for some time. It is thus very important to find the correct price at which an investor feels comfortable with buying. It is important to not buy too late when the price has already began to climb, but buying too early could also prove to be a painful decision. With so many differing opinions flying about and nobody really knowing for sure where oil prices will be six months from now, investors interested in taking a chance at buying oil should consider finding ways to hedge their bets.

In the long run it is highly likely that prices for oil will once again go up. Although many analysts’ believe that prices could remain low for an extended period of time, simple economics dictate that at some point prices will rise. Whether this will be this summer when travel traditionally increases or at some other point in the future continues to be unknown, but eventually oil prices will be stipulated by increasing demand and will increase.

One way for investors looking to get into oil to hedge their bets is by buying long into airlines. Airlines and oil prices have an inverse relationship. When oil prices go up, airlines need to pay more for fuel and thus have lowered profits. When oil prices go down such as they have been doing, airlines benefit from decreased costs and are able to increase their profit line. Buying long on airlines while also owning a long position in oil is one technique that allows an investor to protect what some may deem a dangerous position in a volatile market. Airlines have also been doing very well recently this year even without added benefits from falling oil prices. Travel has continued to increase and airlines are packing more and more flights into the day. Airline stocks also tend to have a stronger correlation with falling oil prices than they do rising. Although airlines do face higher costs when oil prices are high, the change in stock prices associated with an increase in oil prices usually are not as large as when oil prices fall.

In this example, I am going to demonstrate how investing in airlines as a hedge against a long position in oil could have proved beneficial over the past year.

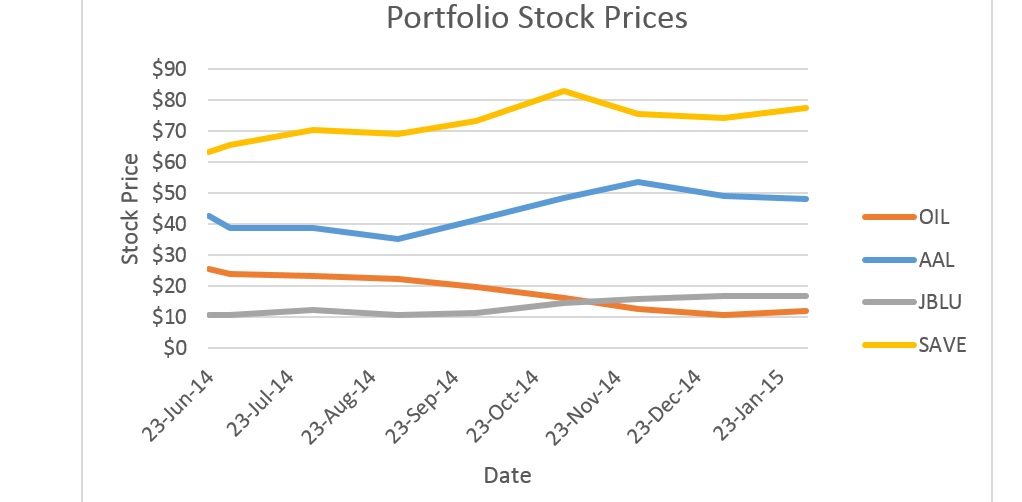

In this case, we have two investors. Both investors have $100,000 invested in a long position in the iPath S&P GSCI Crude Oil TR ETN (OIL). Towards the end of June 2014, when oil prices were at their highest point since September of 2013, and amid speculation about what Saudi Arabia may do with oil, Investor A decided he wanted to protect himself in case oil prices dropped lower. To do this, he decided to hedge 75% of his oil position. This is a large portion to hedge, but he also believed that the stocks were undervalued and liked the airline industry in general. Rather than invest in an airline ETF, he decided to pick four three airlines that he felt had the strongest potential and put $25,000 in each. The three airlines in this situation that our investor chose were American Airlines, JetBlue, and Spirit airlines. Investor B chose to leave his portfolio unaltered as he felt that even if oil prices fell, they would eventually return to higher levels.

If Investor B had owned $100,000 in OIL on June 23rd, 2014 when OIL was priced at $25.69 end of day, and had added $75,000 in OIL rather than using the extra money to hedge, he would have had a February 2cnd portfolio value of $81,306.22, which represents a 54% decline in portfolio value. At this point, Investor B would be facing a massive loss which was only made worse by his decision to not diversify or hedge his portfolio.

If Investor A, had owned $100,000 in Oil on June 23rd, and also $25,000 each in Jet Blue, American Airlines, and Spirit airlines, his portfolio value on February 2cnd would have been $144,462.04 which is only a 17.45% decline in portfolio value. Although Investor A would have seen a negative loss as well, his use of a hedge helped him to greatly decrease the loss.

Investor A’s portfolio since June 23rd would be much more stable and would look like this:

Despite a major fall in the OIL stock price, Investor B was able to limit his losses due to his investments in the three airlines.

As risky a bet as oil is at this moment in time, it is wise to look for a hedge to offset any potential losses from decreasing oil prices.